A regression model ends up with several coefficients that are extremely large in magnitude, making the model unstable and prone to overfitting. Which technique directly addresses this?

Select an answer to reveal the explanation.

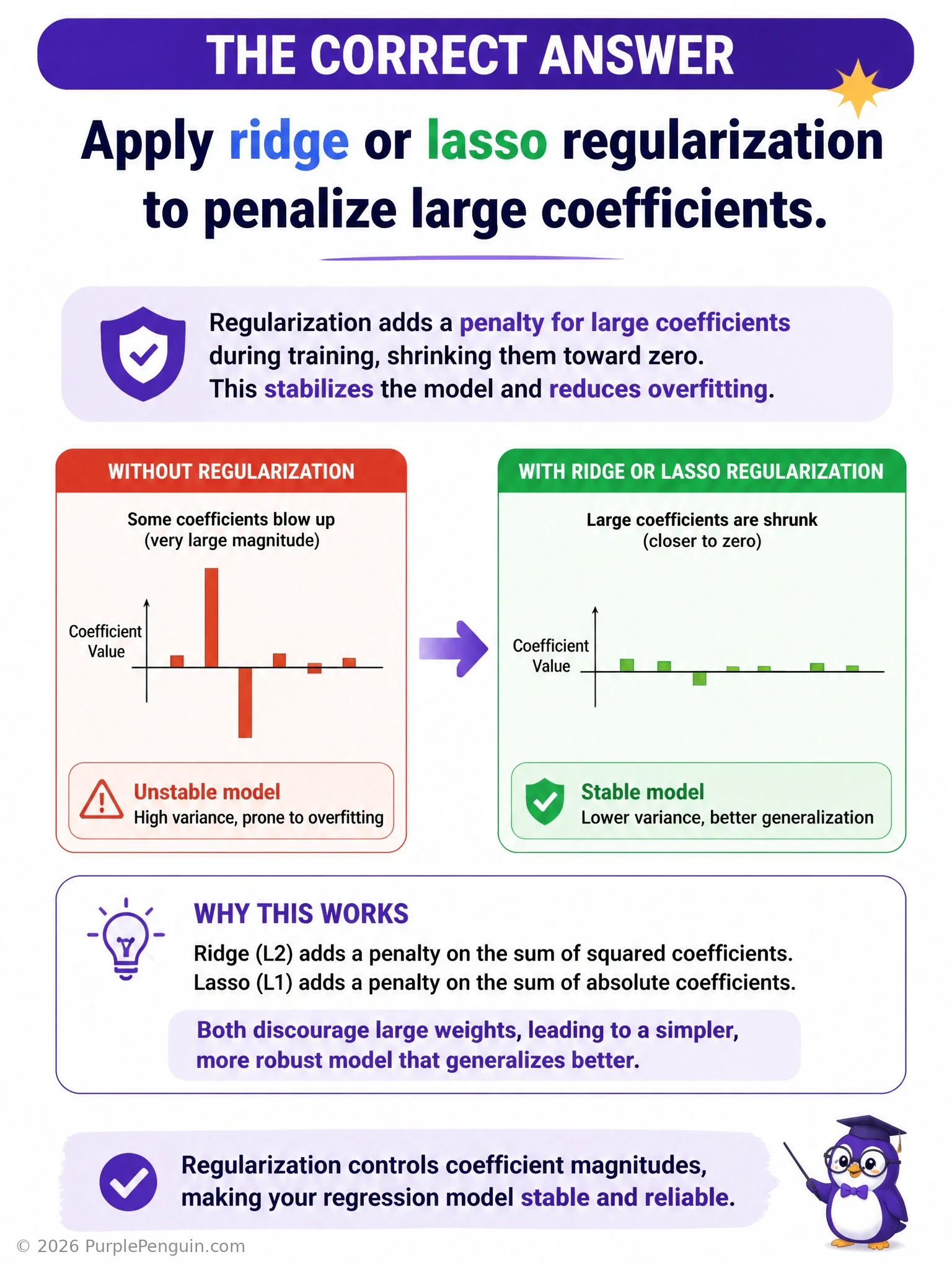

Short Explanation and Infographic

When your coefficients blow up like that, the model is basically leaning way too hard on a few features, chasing every wiggle in the training data. The fix is regularization — ridge (L2) or lasso (L1) — which adds a penalty term to the loss based on the size of the coefficients. Now the model gets punished for having huge weights, so it's nudged toward smaller, more stable values, and generalization improves. Increasing the polynomial degree would make things worse, not better — you're adding complexity and more room for coefficients to swing wildly. Cranking up the learning rate doesn't address coefficient magnitude at all, and a rate that's too large can actually make training diverge. Dropping the intercept just shifts where your line has to pass through the origin — it doesn't constrain the size of the other coefficients one bit.

Full explanation below image

Full Explanation

When a regression model develops excessively large coefficients, it is typically a sign of overfitting: the model is assigning outsized importance to certain features, often to fit noise in the training data, which makes the model highly sensitive to small changes in input and prone to poor generalization. Ridge regression (L2 regularization) addresses this by adding a penalty term proportional to the sum of squared coefficients to the loss function, shrinking all coefficients toward zero (though rarely to exactly zero) and improving stability. Lasso regression (L1 regularization) adds a penalty proportional to the sum of the absolute values of the coefficients, which can shrink some coefficients all the way to zero, effectively performing feature selection alongside shrinkage. Both techniques directly constrain coefficient magnitude, trading a small increase in bias for a meaningful reduction in variance.

Increasing the polynomial degree of the input features is incorrect — and actually counterproductive — because adding higher-order polynomial terms increases model complexity and flexibility, which typically exacerbates overfitting and can produce even larger, more volatile coefficients rather than controlling them.

Switching to a larger fixed learning rate does not address coefficient magnitude; the learning rate controls the step size during optimization and affects convergence speed and stability, but it does not penalize or constrain the final size of the learned weights. In fact, an excessively large learning rate risks causing the optimizer to overshoot and diverge entirely.

Removing the bias/intercept term does not constrain coefficient size either; it merely forces the regression line or hyperplane to pass through the origin, which does nothing to limit how large the slope coefficients on the other features can grow, and can actually degrade fit quality.

A useful memory aid: regularization acts like a leash on the coefficients — ridge keeps every coefficient on a short leash (shrinks them all somewhat), while lasso can yank some coefficients' leashes so short they're pulled to exactly zero (dropping those features entirely).