When establishing a third-party risk management (TPRM) framework, what is the primary objective of conducting risk assessments on external business partners, such as agents, distributors, and suppliers?

Select an answer to reveal the explanation.

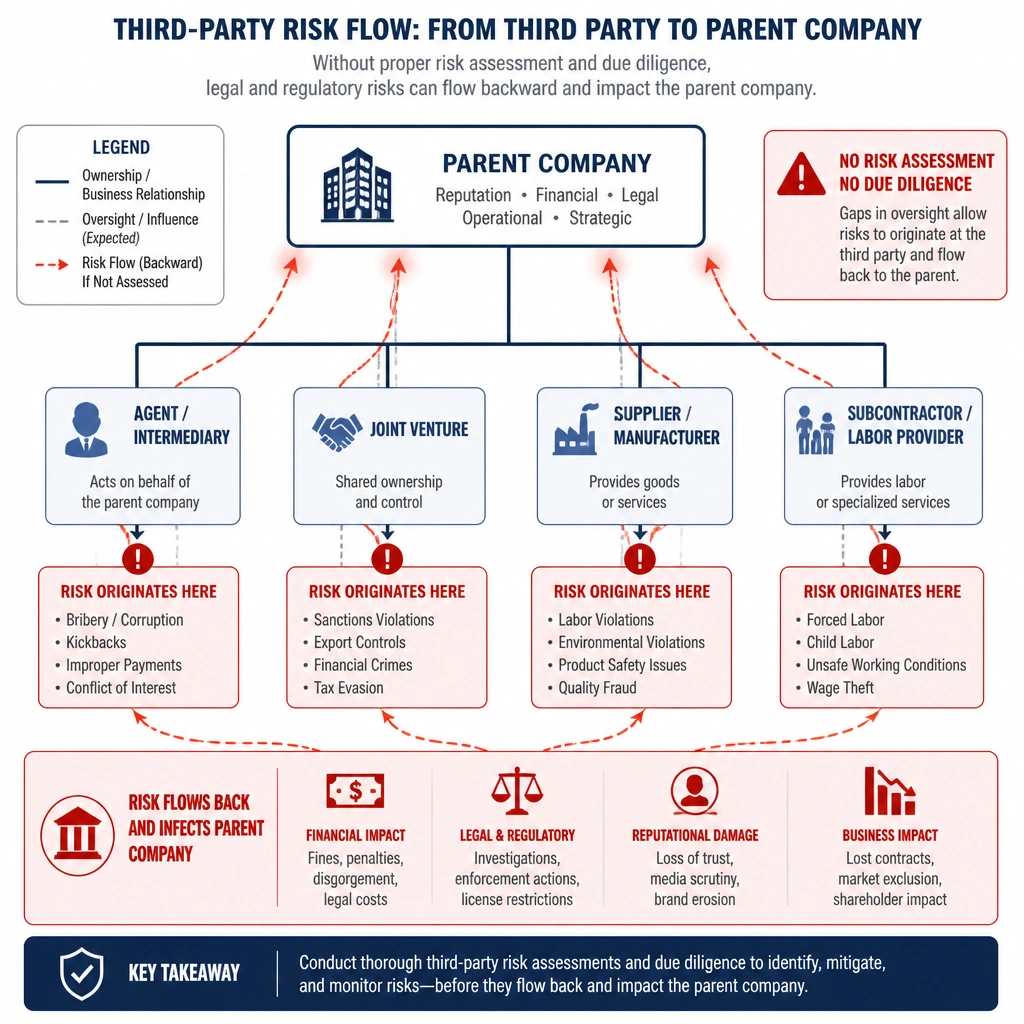

Short Explanation and Infographic

Here's the deal: you can outsource your work, but you can never outsource your risk. If you hire a third-party agent in another country to help you win a contract, and that agent hands a suitcase of cash to a government official, guess who is going to jail? You are. Under laws like the FCPA, the actions of your third-party partners can stick to your company like glue. That's why third-party risk assessments are a big deal. You have to vet these partners before you sign the contract to see if they have a history of bribery, poor internal controls, or regulatory issues. If they do, they're a ticking time bomb for your organization.

Full explanation below image

Full Explanation

Third-party risk management (TPRM) is a critical component of any effective compliance program. Under international anti-corruption frameworks, such as the Foreign Corrupt Practices Act (FCPA) and the UK Bribery Act, organizations are frequently held criminally liable for the corrupt acts of their intermediaries, agents, joint venture partners, and distributors. Therefore, conducting comprehensive due diligence and risk assessments on these entities is not optional; it is a regulatory necessity.

Option B is correct because the primary purpose of a third-party risk assessment is to evaluate the risk of compliance violations, legal liability, or reputational damage that a third party's actions could bring upon the organization. This assessment determines the level of due diligence required, the compliance clauses needed in the contract, and the ongoing monitoring activities necessary to mitigate those risks.

Option A is incorrect because while payroll tax compliance is important, auditing a third party's internal payroll is typically not the primary objective of a standard compliance risk assessment for external partners.

Option C is incorrect because invoice processing and timely payment are operational accounting tasks, not compliance risk management functions designed to detect regulatory exposures.

Option D is incorrect because sourcing the cheapest provider is a procurement or supply chain optimization goal, which is separate from the compliance risk assessment process.