During an internal audit, a compliance officer discovers that several employees suspected a major accounting fraud but chose not to report it to the helpline because they feared immediate termination by their department manager. This scenario highlights a critical weakness in which compliance program element?

Select an answer to reveal the explanation.

Short Explanation and Infographic

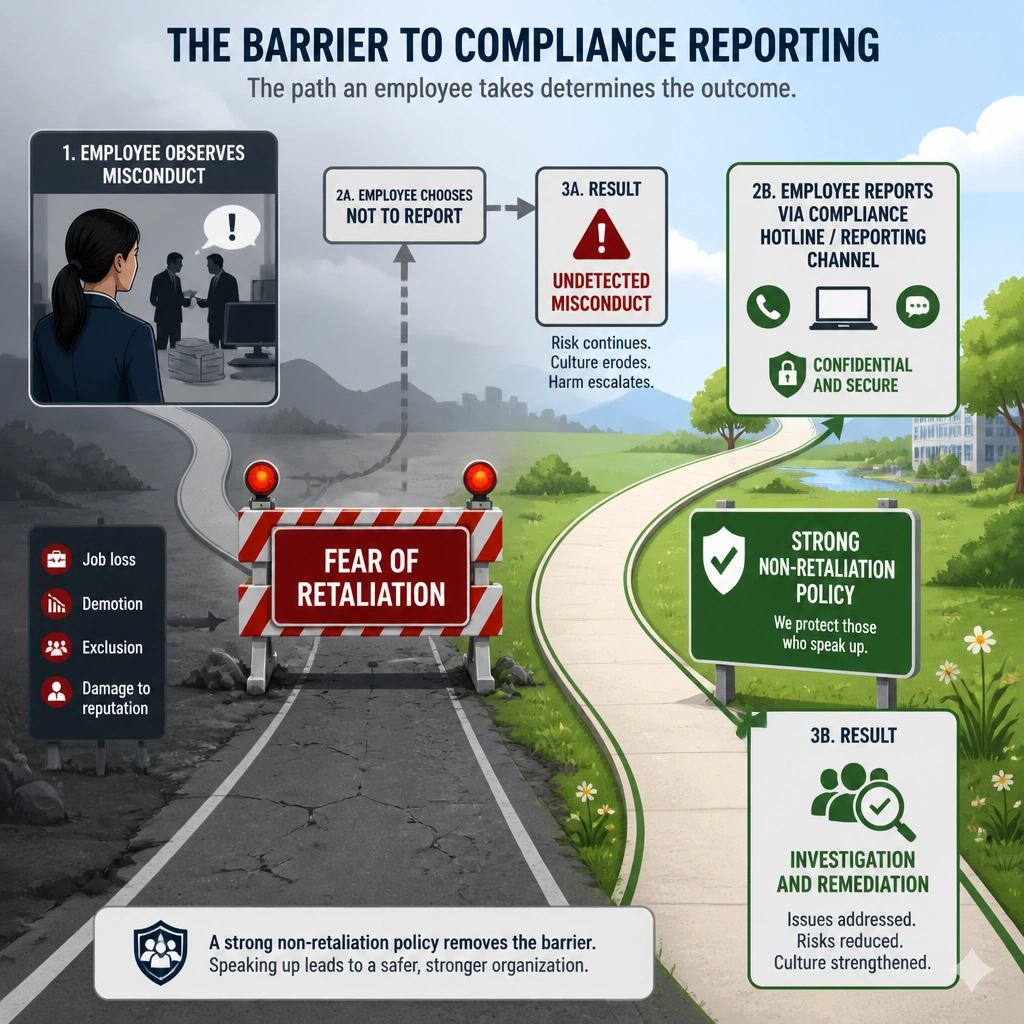

Imagine you're walking through the office and you see a colleague doing something completely illegal. You want to report it, but you're terrified that if you do, your manager will find out and fire you on the spot. So, you keep your mouth shut. That is a massive red flag for any compliance program! It doesn't matter how fancy your hotlines or compliance software are if your employees are too scared to use them. An effective compliance program must have a rock-solid, actively communicated non-retaliation policy. If people don't trust that the company has their back when they raise a concern, the ethical culture is broken, and serious misconduct will stay buried.

Full explanation below image

Full Explanation

An effective compliance program is built on the willingness of employees to report misconduct without fear of reprisal. A "speak-up" culture is one of the key indicators of a healthy compliance environment, and it is heavily emphasized by regulatory frameworks globally, including the U.S. Department of Justice (DOJ) guidelines and the Sarbanes-Oxley Act. If employees observe violations of the code of conduct or legal standards but remain silent due to fear of retaliation, the program's reporting mechanisms are rendered useless.

Option C is correct because the fear of termination for reporting misconduct is a direct symptom of a weak non-retaliation policy or a failure to cultivate an ethical culture where employees feel safe speaking up. Organizations must not only publish a non-retaliation policy but also actively enforce it, discipline managers who retaliate, and demonstrate to the workforce that reporting is protected and valued.

Option A is incorrect because while accounting fraud itself represents a failure of financial controls, the employee's hesitation to report the observed fraud is a failure of the reporting and ethical culture, not the financial systems.

Option B is incorrect because third-party due diligence deals with managing risks associated with external vendors, suppliers, and agents, which is unrelated to internal employee reporting dynamics.

Option D is incorrect because the issue is not the methodology of identifying risks (the risk assessment), but rather the cultural barrier preventing employees from utilizing established channels to report active misconduct.