When establishing an organizational compliance framework, how should a compliance officer design the risk assessment process to ensure its long-term viability and effectiveness?

Select an answer to reveal the explanation.

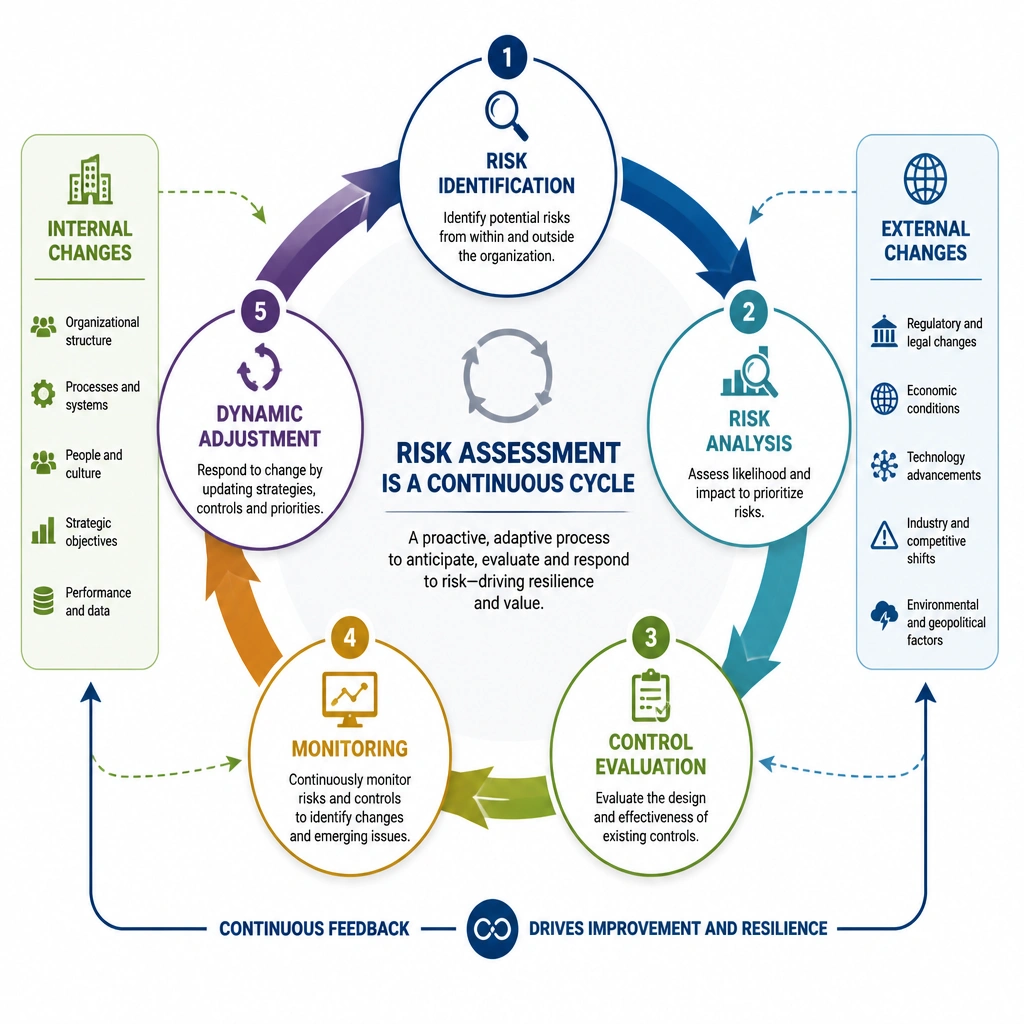

Short Explanation and Infographic

Think of risk assessment like the GPS on your car dashboard. If you only update the map once when you buy the car, and then drive around for five years, you're going to get seriously lost! Roads change, construction pops up, and new detours appear. That's why risk assessment can't be a one-and-done project (Option A). The business world moves fast—new regulations, new products, mergers, and external threats show up every single day. If your risk assessment isn't continuous and dynamic, you're operating with blinders on in a fast-moving storm. The correct answer is C. You've got to keep evaluating and adapting to keep the program alive. And don't make the rookie mistake of only looking at financial risks (Option B) or leaving it entirely to external auditors (Option D) who don't know your day-to-day operations. You must own this process internally, keep it rolling, and adjust as your company grows.

Full explanation below image

Full Explanation

The correct answer is C. A risk assessment is not a static document or a one-time event; it is a foundational, continuous process. Ethics and compliance standards, including the ISO 37301 compliance management systems standard and the US Department of Justice (DOJ) guidelines, emphasize that risk assessments must be updated regularly to reflect changes in an organization's size, operational structure, geographic footprint, and regulatory environment. A static risk assessment quickly becomes obsolete as mergers and acquisitions, new product launches, structural shifts, or geopolitical developments introduce entirely new risk vectors.

Let's analyze why the other options are incorrect: - Option A is incorrect because treating risk assessment as a static, one-time exercise fails to capture new, evolving risks that emerge after the initial program design. This creates a false sense of security and leaves the organization blind to new regulatory requirements. - Option B is incorrect because restricting the scope of risk assessment to financial and accounting controls ignores crucial non-financial compliance risks. An effective compliance program must cover areas such as anti-bribery and corruption (ABAC), data privacy, environmental regulations, health and safety, and trade sanctions. - Option D is incorrect because while external consultants and auditors can provide valuable support and objectivity, the internal compliance function and business leaders must actively own and participate in the risk assessment. Internal teams possess the operational knowledge required to identify hidden compliance issues and cultivate a strong compliance culture.

Ultimately, a dynamic and continuous risk assessment process allows compliance teams to allocate resources efficiently, preempt emerging compliance threats, and demonstrate the effectiveness of the program to external regulators.