An organization has designed and implemented a comprehensive set of compliance policies and training modules. However, the Chief Compliance Officer insists on scheduling ongoing monitoring and auditing activities. What is the primary business and regulatory justification for this requirement?

Select an answer to reveal the explanation.

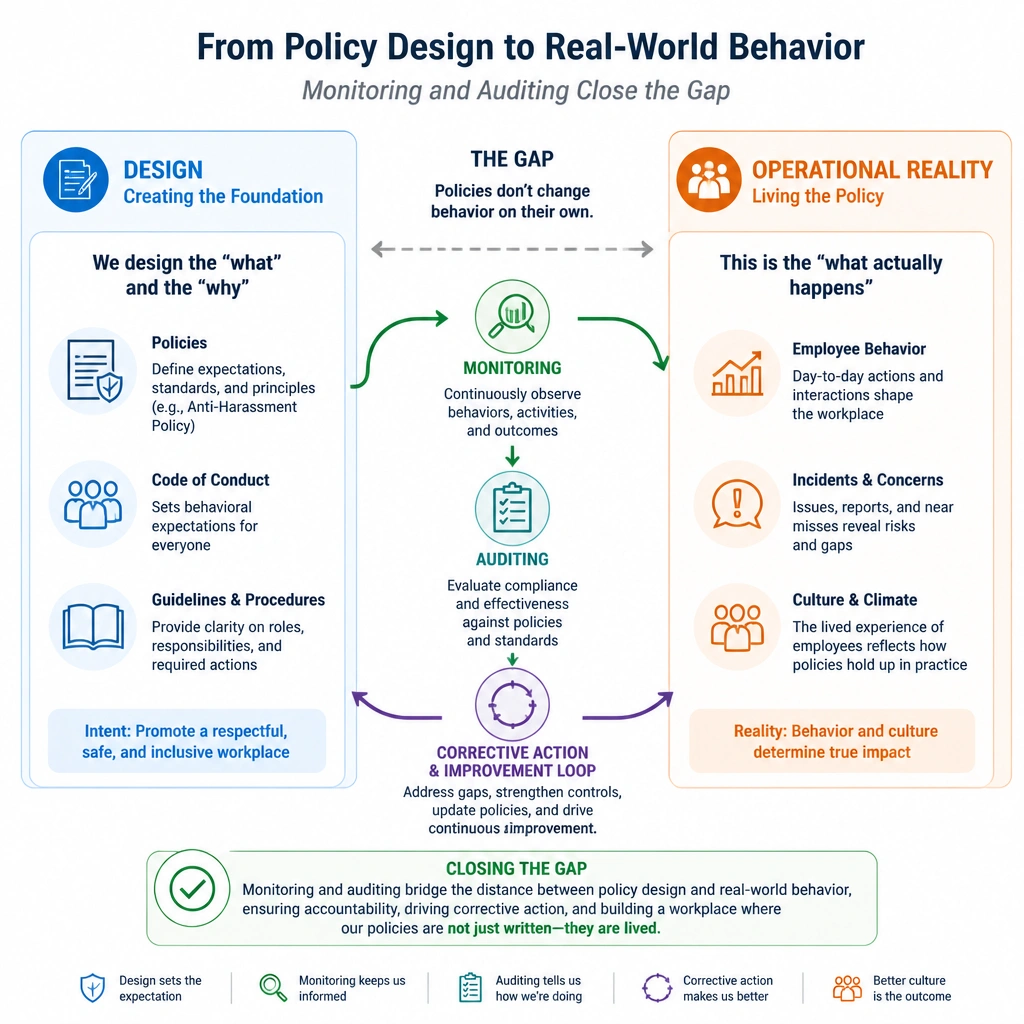

Short Explanation and Infographic

Here's the deal: you can write the most beautiful compliance policies in the world, but if nobody is actually following them, they're just expensive paperweights. Think of auditing and monitoring like running network diagnostics. You don't just set up a router and hope it works forever; you monitor traffic, run tests, and check for bottlenecks. Auditing is your deep dive to see if your controls are actually working in the real world. Monitoring is your daily check. Together, they tell you if your program is doing its job and where you need to patch things before a regulator knocks on your door. Options A, B, and C are just noise—auditing isn't about feeding consultants or padding budgets. It's about protecting the business and staying ahead of new risks. Got it? Sweet.

Full explanation below image

Full Explanation

Designing a compliance program is only the first step; ensuring its operational effectiveness requires continuous oversight. Regulators, including the U.S. Department of Justice (DOJ) in its guidance on the "Evaluation of Corporate Compliance Programs," evaluate whether a program is implemented in good faith and whether it actually works in practice. This determination cannot be made without robust, structured monitoring and auditing mechanisms.

Let's analyze the differences between these options: - Option D is correct because monitoring and auditing provide empirical evidence of whether internal controls are functioning as intended. Monitoring refers to real-time, ongoing checks of day-to-day operations (e.g., tracking training completion rates or hotline reports), while auditing is a retrospective, independent review designed to assess the adequacy and compliance of specific business units or processes. Together, they allow the organization to identify control failures, adapt to emerging regulatory threats, and implement timely corrective actions. - Option A is incorrect because third-party management of internal finances is a governance model decision, not the purpose of compliance monitoring or auditing. Compliance functions oversee compliance with rules, rather than outsourcing corporate financial management. - Option B is incorrect because compliance auditing is designed to protect organizational value and prevent legal liabilities, not to artificially increase operational overhead or turnover. - Option C is incorrect because while external consultants may be leveraged for independent audits, the objective of the program is self-correction and risk mitigation, not generating billable hours for third parties.

Regular audits verify that the organization's ethical culture is strong and that policies are being adhered to across all levels of the enterprise.