A quant team wants to forecast next-day closing prices using several years of daily historical price and volume data. Which type of architecture is best suited to this time-series prediction task?

Select an answer to reveal the explanation.

Short Explanation and Infographic

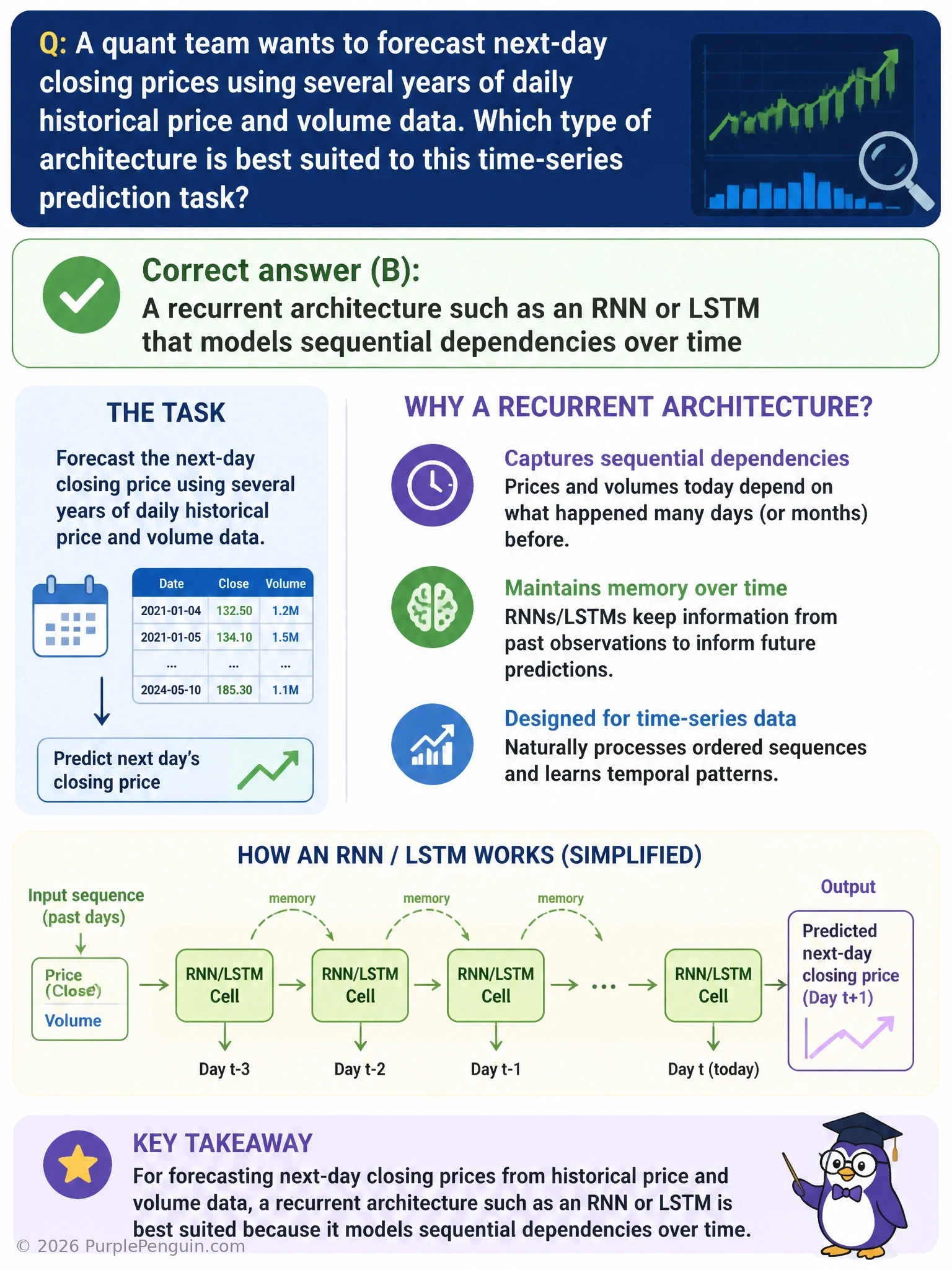

For forecasting a time series like stock prices, you want an architecture built to remember order and sequence, that's an RNN or, better yet, an LSTM. These networks carry a hidden state forward through time, so today's prediction can be informed by patterns built up over the last several weeks or months of prices, not just today's isolated numbers. A plain feedforward network treats every day as a brand-new, unrelated example, which throws away exactly the temporal structure you're trying to exploit. A convolutional autoencoder is built for reconstructing spatial structure in images, not modeling sequences over time. And a GAN is a generative model for creating new synthetic samples that resemble a distribution, it's not designed for supervised sequential forecasting. LSTM or RNN is the right call here.

Full explanation below image

Full Explanation

Recurrent Neural Networks (RNNs), and especially their more capable variant, Long Short-Term Memory networks (LSTMs), are purpose-built for sequential data where the order of observations carries meaningful information, which is precisely the case with time-series data like daily stock prices and trading volumes. These architectures process a sequence one time step at a time while maintaining an internal hidden state that is updated at every step, allowing information from earlier time steps to influence how later inputs are interpreted. LSTMs specifically add gating mechanisms, the input, forget, and output gates, that let the network selectively retain, discard, or expose information over long time horizons, making them well-suited to captures trends, momentum, and seasonality patterns that unfold over many days or weeks, which are common features in financial time series.

The feedforward-network distractor is incorrect because a standard feedforward network with no recurrent or temporal structure processes each input independently, with no built-in mechanism to relate today's features to the sequence of prior days; while such a network could take a fixed window of past days as concatenated input features, it does not naturally scale to variable-length histories or capture the same fine-grained sequential dependencies that recurrent architectures learn implicitly. The convolutional-autoencoder distractor is incorrect because autoencoders, and especially convolutional variants applied to images, are designed to learn compressed representations for reconstruction, a task suited to spatial data such as pixel grids, not to supervised forecasting of the next value in a numeric sequence; it lacks a natural forecasting output and is oriented toward unsupervised representation learning rather than prediction. The GAN distractor is incorrect because generative adversarial networks are designed to learn a data distribution well enough to generate novel synthetic samples resembling that distribution, useful for tasks like synthetic data augmentation, but they are not the standard choice for direct supervised next-step prediction on a real, specific time series, since their generator has no built-in supervised loss tied to matching actual future values.

A useful memory aid: whenever 'order matters' and history should inform the next prediction, whether in language, audio, sensor streams, or financial time series, recurrent architectures like RNNs and LSTMs (or, in modern practice, attention-based sequence models) are the natural fit, while feedforward, convolutional, and generative architectures serve fundamentally different data structures and objectives.