A financial services company is designing its internal compliance program. The Chief Compliance Officer explains the role of internal controls to the board. What is the fundamental, primary objective of these internal controls?

Select an answer to reveal the explanation.

Short Explanation and Infographic

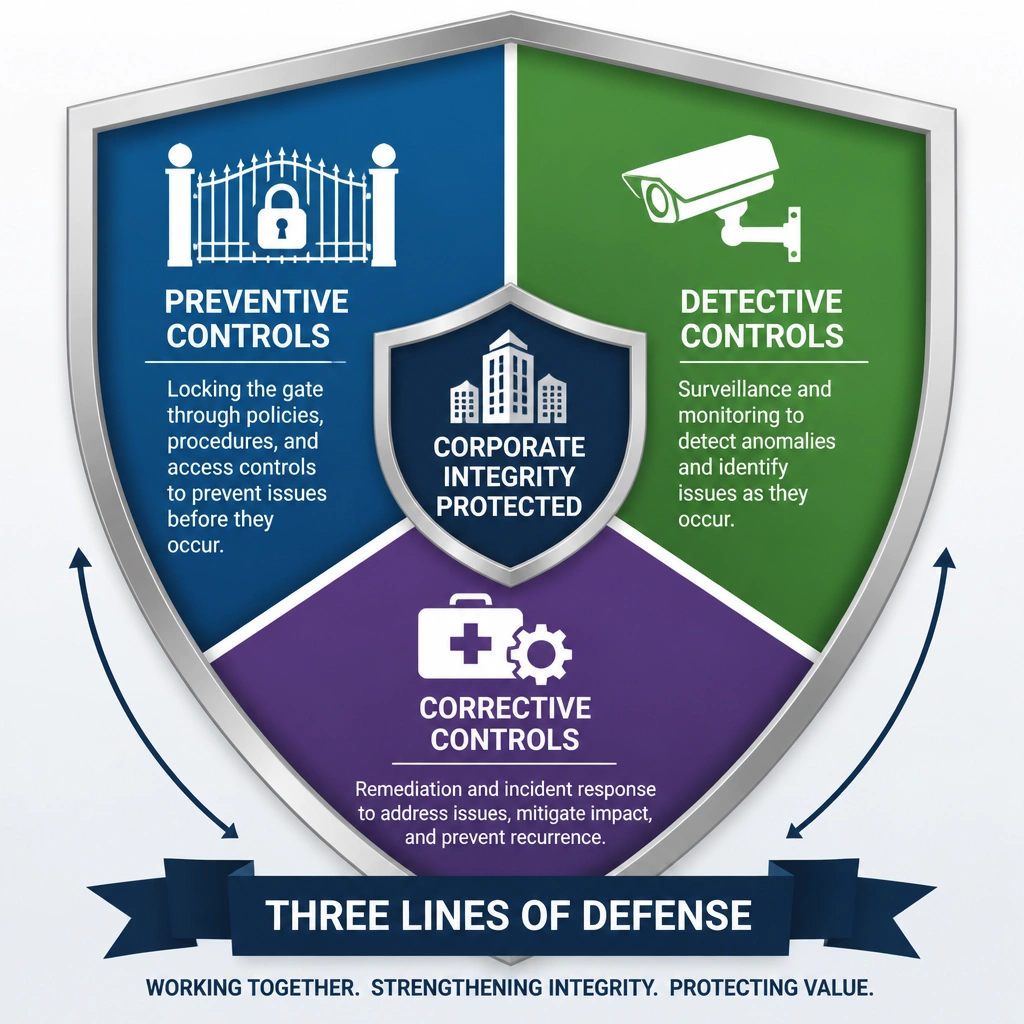

Think of internal controls like the access control lists (ACLs) and firewalls on your network. Why do we put them there? Simple: to prevent bad traffic from getting in, detect if something sneaky did get through, and give us a way to clean up the mess. That's exactly what internal controls do for business processes. They are your safeguards. If you answered A, you nailed it. They keep the business running clean by stopping mistakes before they happen, catching them if they do, and fixing them fast. Got it? Let's keep rolling.

Full explanation below image

Full Explanation

Internal controls are processes, policies, and systems designed to provide reasonable assurance regarding the achievement of objectives in operational effectiveness, financial reporting reliability, and compliance with laws and regulations. The COSO (Committee of Sponsoring Organizations of the Treadway Commission) framework categorizes internal controls into preventive, detective, and corrective controls, which work together to safeguard assets and ensure compliance. Option A is correct because the ultimate objective of an internal control framework is to prevent non-compliance and operational errors before they occur (preventive), detect them quickly if they do occur (detective), and establish mechanisms to remediate and correct the issues (corrective). This three-tiered approach ensures that risks are managed within the organization's risk appetite. Option B is incorrect because internal controls are the responsibility of the organization's management, not the external auditors. External auditors assess the effectiveness of controls but do not assume the company's liability or risk. Option C is incorrect because internal controls are designed to guide and constrain operations to ensure compliance, not to make strategic business decisions or replace the executive team. Option D is incorrect because internal controls are meant to enhance operational efficiency and protect value, which supports profitability rather than seeking to reduce it.