A multinational corporation is onboarding a foreign logistics provider to handle customs clearance in a region known for high corruption risks. Why should the compliance officer conduct a comprehensive third-party risk assessment before finalizing the contract?

Select an answer to reveal the explanation.

Short Explanation and Infographic

Check this out: when you hire a third-party vendor, their mistakes become your compliance nightmares. Imagine your boss walks in and says, "Hey, that customs broker we hired just paid off a foreign official, and now the DOJ is at our door!" Not a conversation you want to have, trust me. A third-party risk assessment isn't about saving a buck or checking their payroll; it’s about figuring out if their actions are going to drag your company into a massive regulatory mess. You’ve got to protect your organization by evaluating their risk profile before you sign on the dotted line. Got it? Sweet. Let's keep rolling.

Full explanation below image

Full Explanation

A third-party risk assessment is a critical component of an effective compliance program. Under major regulatory frameworks such as the Foreign Corrupt Practices Act (FCPA) and the UK Bribery Act, organizations can be held directly liable for the corrupt activities of their agents, consultants, and suppliers. Therefore, the primary objective of assessing third-party risk is to proactively identify, evaluate, and mitigate the potential legal, financial, and reputational exposures that a vendor's misconduct could bring to the company.

Let's analyze the options to see why the correct answer stands out. The correct option is C. It correctly identifies the core risk management objective: identifying compliance violations, such as bribery, money laundering, or data privacy breaches, that a third party might commit while acting on the company's behalf. Option A is incorrect because verifying financial stability and ensuring timely payment, while important for general supply chain management and procurement, is not the primary focus of a compliance-focused third-party risk assessment. Option B is incorrect because finding the cheapest provider is a commercial or sourcing objective, not a compliance or risk-management goal. In fact, selecting the lowest-bid vendor without proper vetting often increases compliance risks rather than reducing them. Option D is incorrect because auditing internal payroll processes is an administrative function of the human resources and finance departments, completely unrelated to evaluating the compliance risk posed by external third-party relationships.

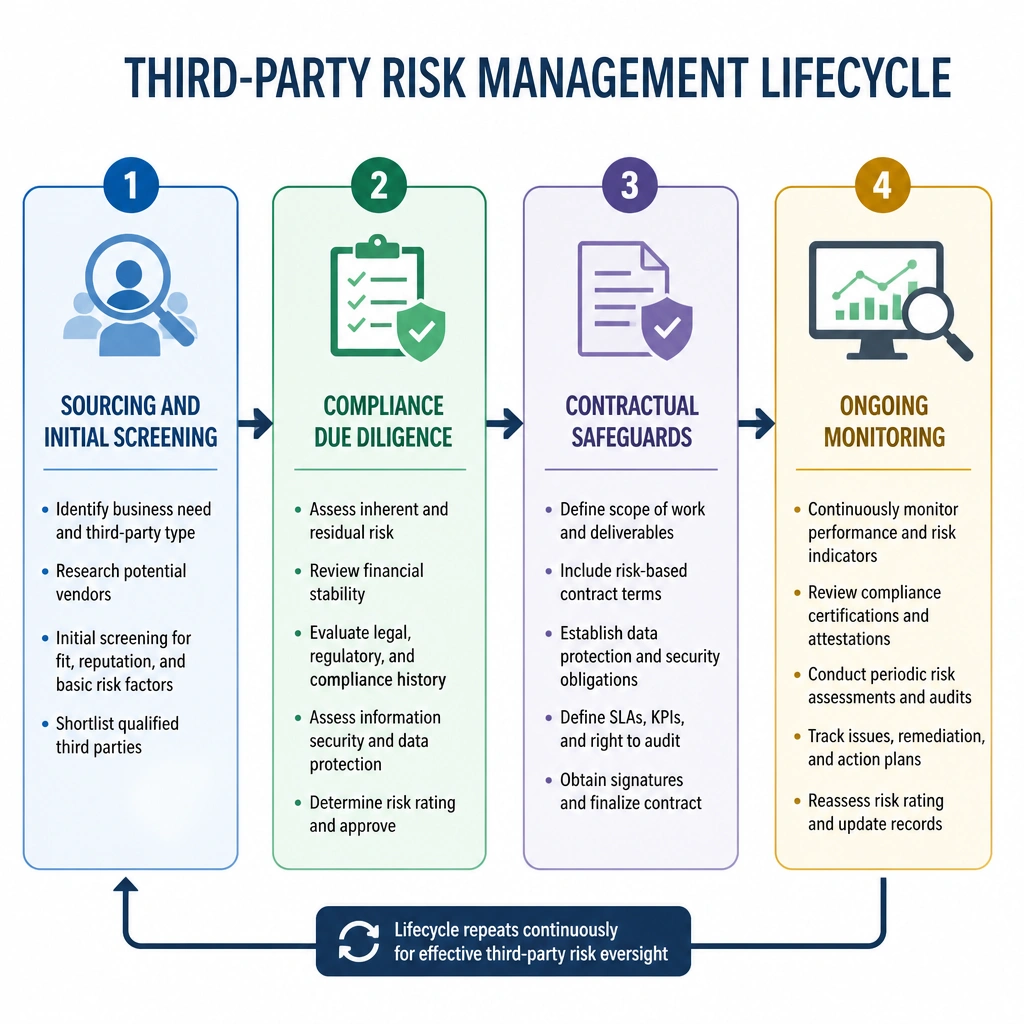

In practice, a robust third-party risk management program involves initial screening, detailed due diligence questionnaires, database searches for politically exposed persons (PEPs) or sanctions, contractual compliance clauses, and ongoing monitoring to ensure the vendor continues to operate ethically.