In a corporate compliance framework, what is the primary objective of establishing and maintaining a system of internal controls?

Select an answer to reveal the explanation.

Short Explanation and Infographic

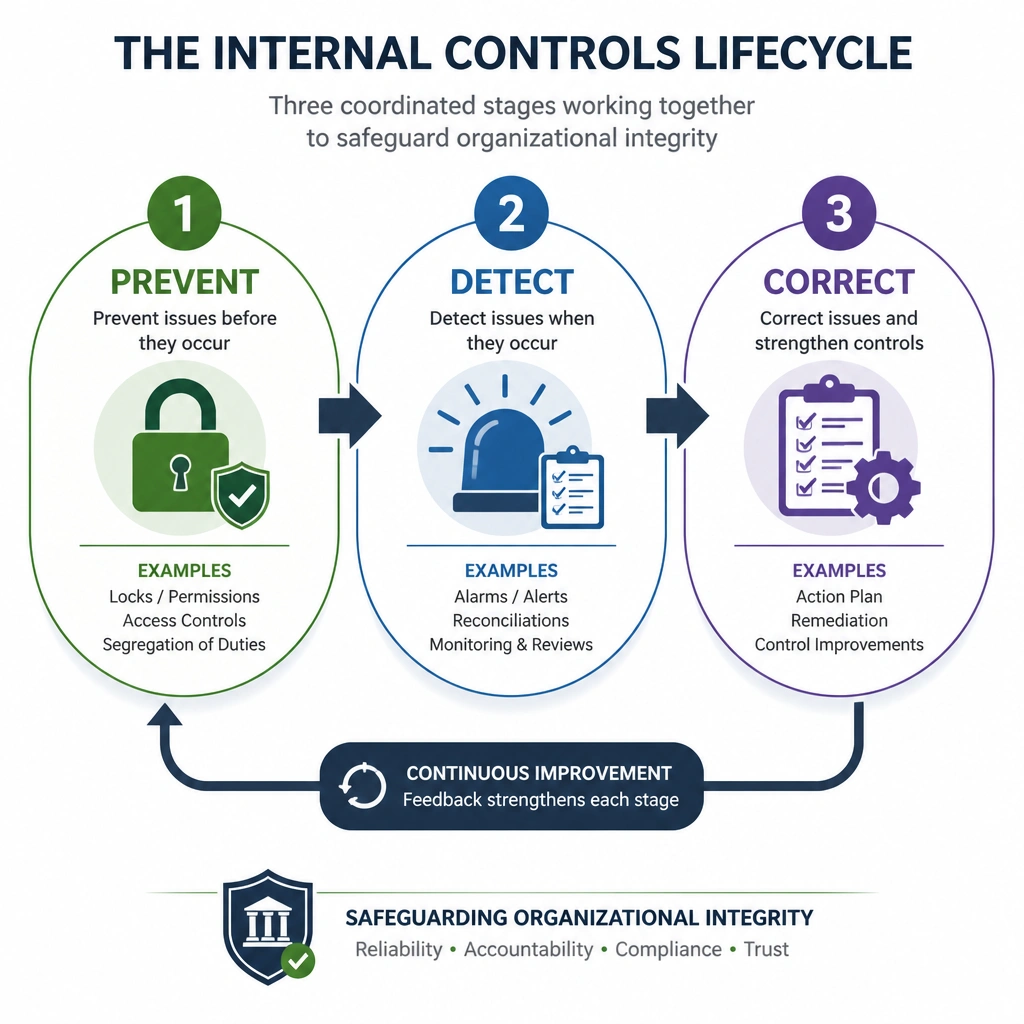

Think of internal controls like the guardrails and warning signs on a winding mountain road. They aren't there to stop you from driving, and they certainly don't steer the car for you—that’s management’s job. Their real purpose is to prevent you from flying off the cliff, detect if you start slipping, and help you get back on track. In the compliance world, that means preventing errors, detecting when something goes wrong, and correcting the issue before it turns into a headline-making disaster. Hopefully you answered C! That's because good internal controls—like separation of duties or double-signature requirements—are designed to catch human errors or bad actors before they ruin your day. Got it? Sweet. Let's keep rolling!

Full explanation below image

Full Explanation

The correct answer is C. The fundamental purpose of internal controls within any compliance or financial framework is to provide reasonable assurance that the organization's objectives are met regarding operational efficiency, reliable reporting, and compliance with laws and regulations. To achieve this, internal controls are categorized into three main types: preventive (designed to stop errors or irregularities before they occur, such as segregation of duties), detective (designed to identify errors or irregularities after they have occurred, such as reconciliations or audits), and corrective (designed to remedy problems discovered by detective controls, such as system patches or training).

Option A is incorrect because internal controls do not make business decisions; they establish the boundaries, procedures, and checks within which business decisions must be made by authorized managers. Option B is incorrect because while efficient controls can protect value, their primary purpose is risk mitigation and integrity, not maximizing short-term profits at all costs, which could lead to compliance failures. Option D is incorrect because the presence of internal controls is focused on operational processes throughout the company, not merely ensuring the legal department has resources or capacity for litigation defense.