When an organization operates in a jurisdiction identified as having a high risk of money laundering, which of the following preventive controls is most critical to implement?

Select an answer to reveal the explanation.

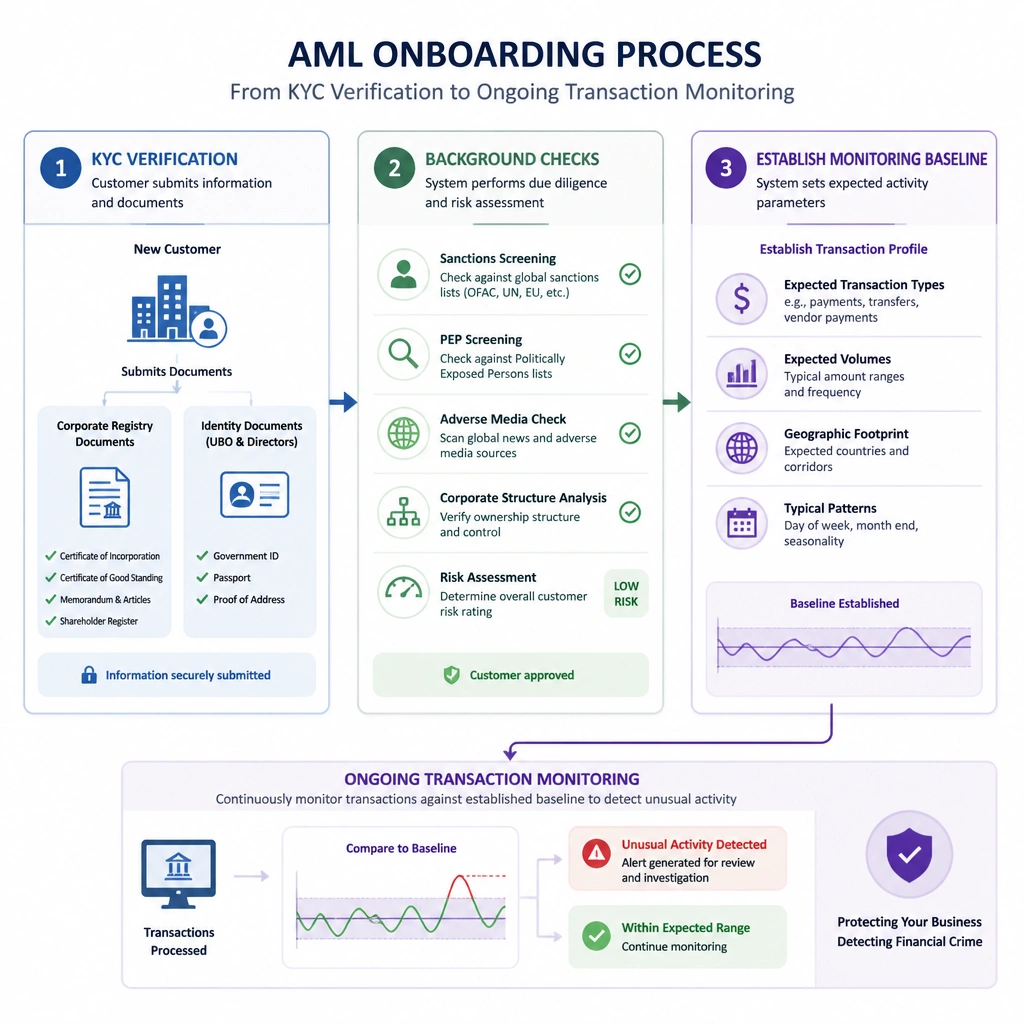

Short Explanation and Infographic

Let me show you how this works in the real world. If you're doing business in a country where money laundering is rampant, you can't just close your eyes and hope for the best. And you definitely shouldn't accept large sacks of cash (Option A)—that's practically inviting the cartel to use your business as a laundry mat! You also don't want a single person approving all transactions (Option B) because that lacks separation of duties and is a massive fraud risk. The correct answer is C. You have to implement 'Know Your Customer' (KYC) procedures. This means you verify exactly who your customers are, where their money comes from, and you track their transactions to flag anything weird. Option D is an extreme business-stopping move that most companies won't do. KYC and tracking give you the shield you need to do business safely in tough neighborhoods.

Full explanation below image

Full Explanation

The correct answer is C. In anti-money laundering (AML) compliance, preventive controls are essential to prevent the organization's financial systems from being used to disguise the origins of illicit funds. The foundational preventive controls are "Know Your Customer" (KYC) and Customer Due Diligence (CDD) procedures. These protocols require the organization to verify the identity of customers, identify beneficial owners, and understand the nature of the business relationship. When combined with ongoing transaction monitoring, the organization can detect deviations from normal behavior and file Suspicious Activity Reports (SARs) as required by global AML regulations (such as the Financial Action Task Force standards).

Let's analyze the incorrect options: - Option A is incorrect because cash transactions are highly anonymous and represent the highest risk factor for money laundering. Accepting unrestricted cash payments is a major compliance failure. - Option B is incorrect because a single person managing all financial transactions violates the principle of segregation of duties, creating a severe operational and fraud risk. - Option D is incorrect because while de-risking (exiting a market entirely) is a choice, it is a commercial strategy rather than a standard compliance control. Organizations can operate in high-risk areas if they deploy proportional risk mitigation measures. Effective AML programs rely on a risk-based approach, applying enhanced due diligence (EDD) to customers in high-risk jurisdictions.