What does the mean absolute error (MAE) metric measure for a regression model?

Select an answer to reveal the explanation.

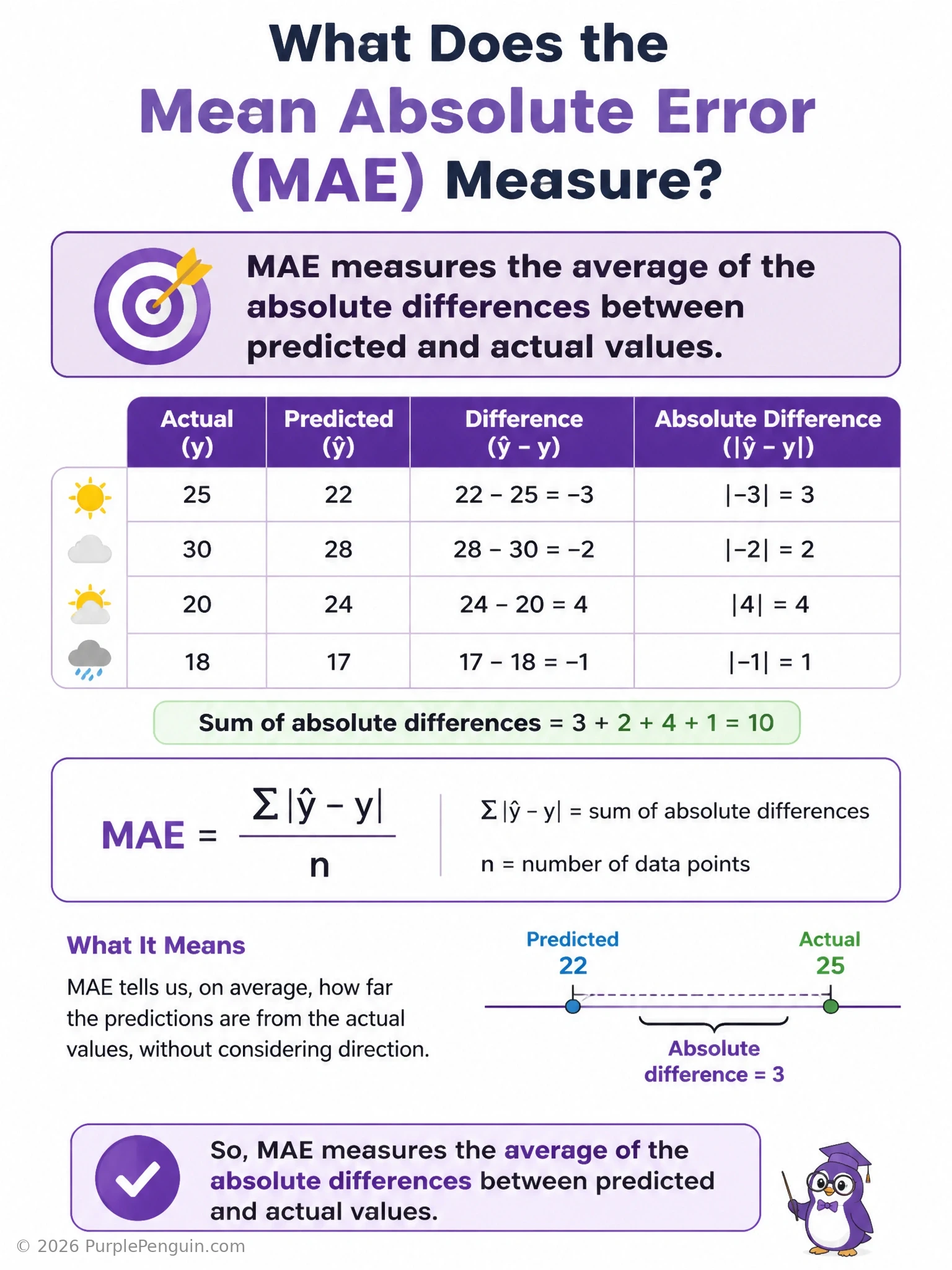

Short Explanation and Infographic

Let's keep this one simple: MAE takes every prediction error, strips off the sign with absolute value, and averages them. That's it — the average of the absolute differences between predicted and actual values. So if your model is off by 2 on one house price and off by 4 on another, MAE just averages 2 and 4. The R-squared option is a totally different animal — that's about explained variance, not raw error size. Squaring the differences instead of taking the absolute value describes MSE, which punishes big misses much harder than MAE does. And "the largest single error" is just describing max error, not an average at all. MAE is prized because it's easy to interpret in the same units as your target and it doesn't let one outlier dominate the score the way MSE does.

Full explanation below image

Full Explanation

Mean absolute error is calculated by taking the absolute value of each prediction's deviation from its true value, summing those absolute deviations, and dividing by the number of samples: MAE = (1/n) * sum(|y_actual - y_predicted|). Because the errors are in absolute value rather than squared, MAE is expressed in the same units as the target variable, which makes it intuitive to communicate to non-technical stakeholders — an MAE of 3.2 on a house-price model in thousands of dollars literally means the model is off by $3,200 on average.

The R-squared distractor is incorrect because R-squared measures the proportion of variance in the dependent variable explained by the model, a goodness-of-fit statistic rather than a raw error magnitude. The squared-differences distractor describes mean squared error (MSE), a related but distinct metric that squares each residual before averaging, which inflates the influence of large errors and makes MSE far more sensitive to outliers than MAE. The largest-single-error distractor describes max error, a worst-case metric that ignores every other prediction in the dataset and therefore doesn't summarize overall performance the way an average-based metric does.

MAE's key practical advantage is robustness to outliers: because errors aren't squared, one wildly bad prediction won't dominate the score the way it would with MSE. This makes MAE a good choice when your data has noisy outliers you don't want to over-penalize, whereas MSE is preferred when large errors are especially costly and should be weighted more heavily. A useful memory aid: MAE = magnitude averaged (linear), MSE = magnitude squared (quadratic penalty).