Imagine you are deploying a machine learning model to detect credit card fraud. Since missed fraudulent transactions (false negatives) cost the company millions in direct losses, the business demands a model that catches as many fraud cases as possible. Which evaluation metric should you prioritize to minimize these costly misses?

Select an answer to reveal the explanation.

Short Explanation and Infographic

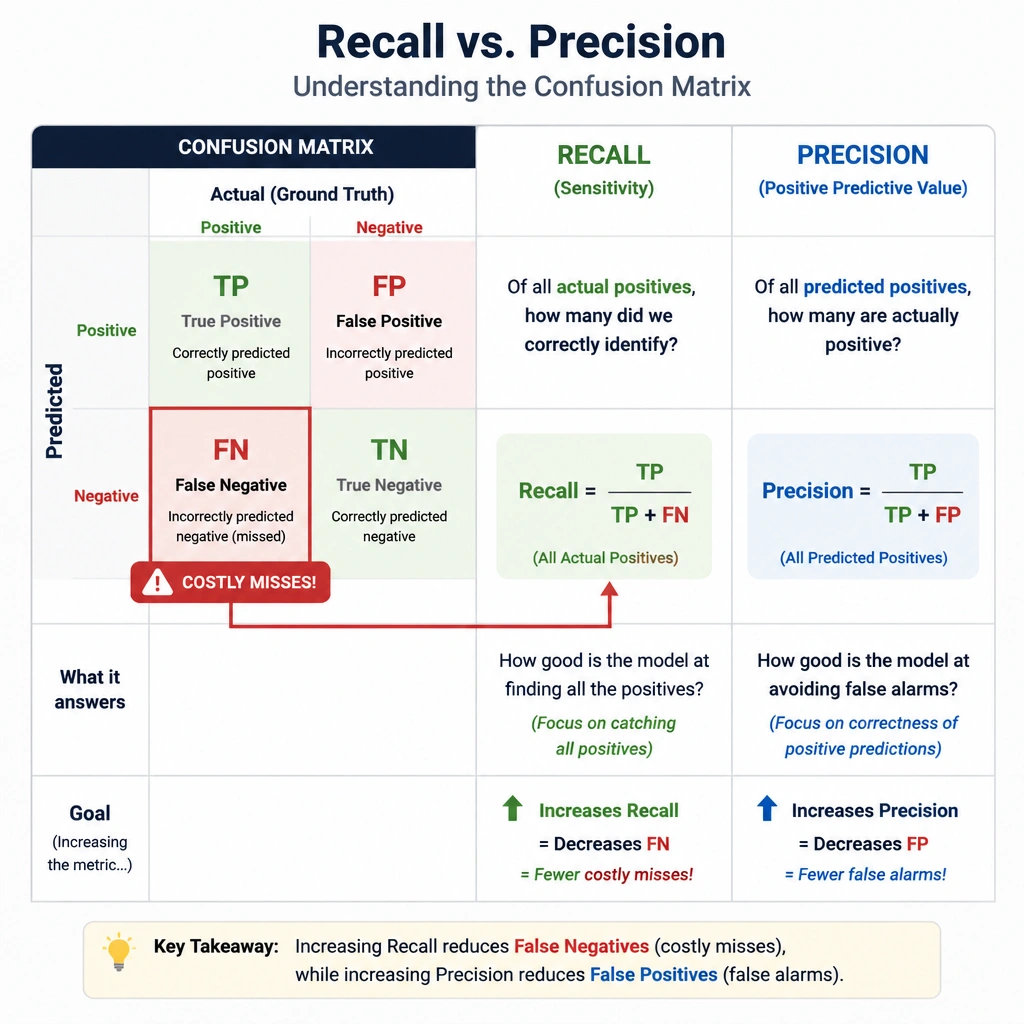

Here's the deal: if a fraudulent transaction slips past our system, that's a false negative. The customer is mad, the bank loses money, and your boss is breathing down your neck. We want to catch every single bad guy, even if we occasionally flag a legitimate transaction by accident. That is what recall is all about. It measures our ability to find all the actual positive cases (the fraud). Precision is different—it's about making sure that when we say something is fraud, we're right. But in this case, we care way more about not missing any fraud. So recall is your gold standard here. Got it? Sweet. Let's keep rolling.

Full explanation below image

Full Explanation

In classification tasks, the choice of evaluation metric is driven by the business consequences of different types of errors: False Positives (FP) and False Negatives (FN). In a fraud detection scenario, a False Negative occurs when a transaction is fraudulent, but the model classifies it as normal. This results in direct financial loss and security breaches.

Recall (also known as sensitivity or the True Positive Rate) is mathematically defined as: $$\text{Recall} = \frac{\text{True Positives}}{\text{True Positives} + \text{False Negatives}}$$ Because False Negatives are in the denominator, maximizing Recall directly minimizes False Negatives. A high-recall model will capture most of the actual fraudulent transactions, ensuring they do not go unnoticed.

Let's look at why the other options are not the primary metric to prioritize: - Option A (Precision) measures the proportion of flagged transactions that are actually fraudulent: $$\text{Precision} = \frac{\text{True Positives}}{\text{True Positives} + \text{False Positives}}$$ Optimizing for Precision minimizes False Positives (flagging a normal transaction as fraud). While high precision prevents customer frustration (fewer blocked legitimate cards), a model optimized solely for precision will be very conservative, missing many actual fraud cases because it only flags transactions it is extremely certain are fraudulent. - Option B (Accuracy) is the ratio of correct predictions to total predictions. In fraud detection, the dataset is highly imbalanced (e.g., 99.9% of transactions are legitimate). A naive model that predicts 'normal' for every transaction would achieve 99.9% accuracy but catch 0% of the fraud, making accuracy a misleading and dangerous metric here. - Option D (F1-Score) is the harmonic mean of Precision and Recall. While it is a good metric to balance both concerns, it does not prioritize minimizing false negatives above all else. Additionally, the definition in Option D incorrectly relates the F1-Score to training and inference speeds, which are operational performance metrics, not classification metrics.